5 Key Credit Score Components

A Credit Score is a numerical representation of a person’s creditworthiness based on a bunch of factors. The components of a credit score are:

Payment History

This refers to your track record of making payments on your debts on time. It takes into account whether you’ve paid your bills on time, missed any payments, or have any accounts go to collections.

Credit Utilization/Amounts Owed

This is the amount of credit you’re using compared to the total credit available to you (AKA credit limits). It’s expressed as a percentage. So your total debt amount over your total possible debt or credit limits. For example, if you have 3 credit cards each with a limit of $5000, your total available credit limit is $15k. If your total owed is $6,500 it would be $6,500/$15,000 = 43%. Keeping your credit utilization low (typically below 30%) is generally recommended as it shows responsible credit management. With our example paying your debt down would obviously lower this percentage. However, it may also be possible (though I cannot advise you one way or another), to lower this % by asking for a credit limit increase as well (please only do this if you are not actively using your cards and know you have the restraint not to get into more debt). So if you ask and receive an increase for one of the cards, and get it increased to $10,000 then your total limits increase to $20,000 and your % would go down to $6500/$20000 = 32.5%, thus improving your credit score. Just make sure you don’t then SPEND that extra credit. Please!!

Length of Credit History

This factor considers the length of time you’ve had any type of credit account. This can be any type of credit such as a car loan, credit card, mortgage, loans etc. A longer credit history can positively impact your score, which demonstrates a track record of responsible credit management.

Credit Mix

A diverse mix of credit can be seen as a positive indicator of your ability to manage different types of credit responsibly. This takes into account the types of credit accounts you have, like credit cards, personal or student loans, mortgages, or retail accounts. You’ll hear people talk about “good” (mortgages and student loans) and “bad” (credit cards) credit. In my opinion, any high-interest credit is bad, and student loans are the only loans that won’t be forgiven in bankruptcy, and some of them can be pretty high interest – which doesn’t sound great to me. But if you keep your eyes open you’ll be okay.

New Credit

This refers to any recent credit inquiries or newly opened accounts. Applying for multiple new credit accounts within a short period can have a negative impact on your score. It’s important to be mindful of how frequently you’re seeking new credit. Also be aware that when you purchase a new cell phone and choose a new plan, start a new utility account (gas or electric), or even a new cable tv account, they will often perform what’s called a credit ‘inquiry’. These all count as ‘new credit’ requests. If you’re going to make a big purchase, make sure you make the purchase or at least apply for the credit first before these hit your credit.

Public Records and Collections:

This factor considers any negative information on your credit report, such as bankruptcies, tax liens, or accounts in collections. These can significantly impact your credit score in a negative way.

Credit records refresh/fall off after about 7 years. Everyone in the US is entitled to a free credit report each year that reports one credit score and lists each company and how they are reporting your payment history. It’s a good idea to check it for accuracy, and if you find errors there’s a way to report them to the bureaus on the site. https://www.freecreditreport.com

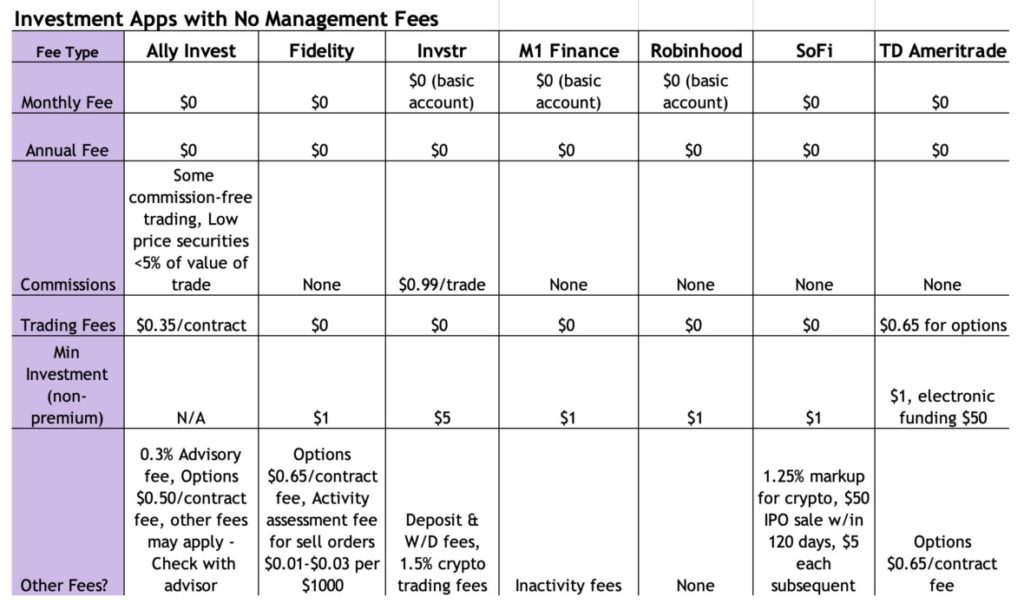

Read Next: Top Ten Beginner-Friendly Investing Apps